Words of Wisdom:

"Testosterone makes the world go round."

- Shaundsp23

Indian Fmcg

- Date Submitted: 03/07/2013 01:32 AM

- Flesch-Kincaid Score: 54.8

- Words: 9412

- Essay Grade: no grades

- Report this Essay

22 August 2012

Asia Pacific/India

Equity Research

Consumer Staples / OVERWEIGHT

India Consumer Sector

Research Analysts

Arnab Mitra

91 22 6777 3806

arnab.mitra@credit-suisse.com

Akshay Saxena

91 22 6777 3825

akshay.saxena@credit-suisse.com

INITIATION

Premium rush

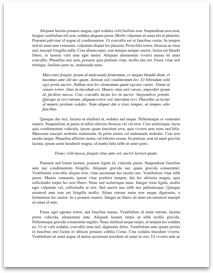

Figure 1: GSK, Emami, Marico, ITC and GCPL have strong growth prospects

HIGH

and lower competitive risks

Emami

GCPL

GSK

Marico

Nestle

Micro divers

Colgate

HUL

ITC

LOW

Dabur

HIGH

Competitive risk

LOW

Source: Company data, Credit Suisse estimates

W e initiate coverage on the Indian FMCG sector. We expect its rich valuations

to sustain, as most of the leading companies will likely deliver 15%-25%

earnings CAGR over FY12-15 while maintaining high capital efficiencies. We

initiate on ITC, Godrej Consumer, Emami, GSK Consumer, Marico and HUL

with OUTPERFORM, Nestle with NEUTRAL, and Dabur and Colgate with

UNDERPERFORM ratings.

Focus on micro over macro. Companies in our coverage universe

cumulatively operate in over 25 categories, which have stark divergence in

growth potential as they are at varying stages of penetration, consumption

and premiumisation. We expect categories like skin care, shampoos,

insecticides, hair oils, packaged foods and new segments including face

washes and deodorants to outgrow the broad FMCG market. Companies

with leading brands in these categories are likely to gain the most. GSK,

Marico, GCPL, Emami and Nestle have the best positioned portfolio.

Companies with dominant positions to show margin resilience. W e use

a framework to assess the brand dominance of various companies analysing

each brand in their portfolio. We believe ITC, GSK, Marico, GCPL and

Emami have the highest margin resilience and scope for margin expansion.

Positive on managements investing in innovation and execution

capabilities. Managements at ITC, HUL, GCPL, GSK, Marico and Emami

have upped their investments in brand...

Asia Pacific/India

Equity Research

Consumer Staples / OVERWEIGHT

India Consumer Sector

Research Analysts

Arnab Mitra

91 22 6777 3806

arnab.mitra@credit-suisse.com

Akshay Saxena

91 22 6777 3825

akshay.saxena@credit-suisse.com

INITIATION

Premium rush

Figure 1: GSK, Emami, Marico, ITC and GCPL have strong growth prospects

HIGH

and lower competitive risks

Emami

GCPL

GSK

Marico

Nestle

Micro divers

Colgate

HUL

ITC

LOW

Dabur

HIGH

Competitive risk

LOW

Source: Company data, Credit Suisse estimates

W e initiate coverage on the Indian FMCG sector. We expect its rich valuations

to sustain, as most of the leading companies will likely deliver 15%-25%

earnings CAGR over FY12-15 while maintaining high capital efficiencies. We

initiate on ITC, Godrej Consumer, Emami, GSK Consumer, Marico and HUL

with OUTPERFORM, Nestle with NEUTRAL, and Dabur and Colgate with

UNDERPERFORM ratings.

Focus on micro over macro. Companies in our coverage universe

cumulatively operate in over 25 categories, which have stark divergence in

growth potential as they are at varying stages of penetration, consumption

and premiumisation. We expect categories like skin care, shampoos,

insecticides, hair oils, packaged foods and new segments including face

washes and deodorants to outgrow the broad FMCG market. Companies

with leading brands in these categories are likely to gain the most. GSK,

Marico, GCPL, Emami and Nestle have the best positioned portfolio.

Companies with dominant positions to show margin resilience. W e use

a framework to assess the brand dominance of various companies analysing

each brand in their portfolio. We believe ITC, GSK, Marico, GCPL and

Emami have the highest margin resilience and scope for margin expansion.

Positive on managements investing in innovation and execution

capabilities. Managements at ITC, HUL, GCPL, GSK, Marico and Emami

have upped their investments in brand...

Comments

Express your owns thoughts and ideas on this essay by writing a grade and/or critique.

Sign Up or Login to your account to leave your opinion on this Essay.

Copyright © 2024. EssayDepot.com

No comments